One trend we’ve observed over the past few years is large centralized brands or holding companies that roll up several smaller brands into a local services powerhouse. Advantages include economies of scale by applying shared fixed costs (e.g., back office functions) and quality standards across the board.

Usually, this happens within a given vertical (think: Aspen Dental), as this approach engenders focus and competency in the dynamics of a given service area. For example, in regulated service disciplines like healthcare and finance, focus and competency aren’t just strategic but a compliance issue.

But it’s also happening in home services like HVAC, plumbing, and pest control. And one company demonstrating a version of this roll-up approach is Neighborly. The company has assembled several local brands like Mr. Rooter, Molly Maids, and Mosquito Joe for a broad but focused home-services play.

Neighborly broke down this approach and strategic considerations recently at the Street Fight Live event in Chicago, where Localogy Insider was on hand to capture top takeaways. According to Chief Development Officer, Brad Stevenson, it has rolled up 32 brands in total, spanning 19 service verticals.

Best of Both Worlds

Backing up, Neighborly’s approach is a slightly different flavor of the rollup model seen elsewhere. It has rolled up all those local brands, but not the local services themselves. There, it applies a franchise model, making it a sort of cross between a pure M&A roll-up and a typical franchise-based brand.

This approach has advantages says Stevenson. For example, it can capture the best of both worlds, including economies of scale and fixed resources noted above, while keeping a lighter balance sheet and risk profile as a franchise. There are fewer capital requirements if it doesn’t own all those local shops.

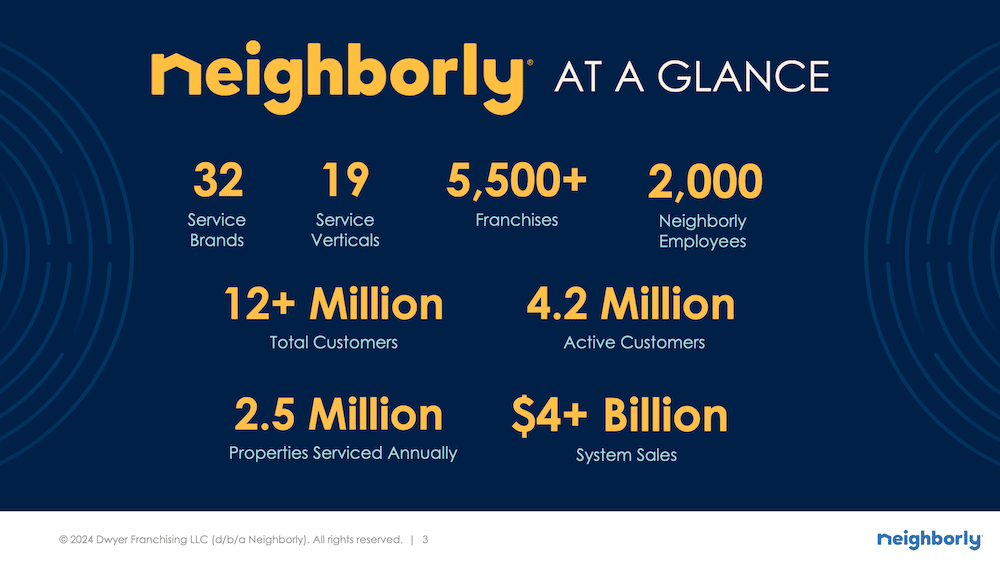

That last part makes it more scalable. In fact, we were surprised at the operational scale that Neighborly has quietly achieved. It currently powers 5,500+ franchises, 2,000 employees, 12 million+ customers, 2.5 million homes serviced annually. In total, $4 billion in gross revenue collectively runs through its system.

To be clear, that’s not $4 billion in revenue for Neighborly, but rather the annual value of services performed under its umbrella. It gets a cut for its branding, marketing, and operational support – again, just like a typical franchise model. But the sheer transaction volume it presides over is still notable.

Revenue Ratcheting

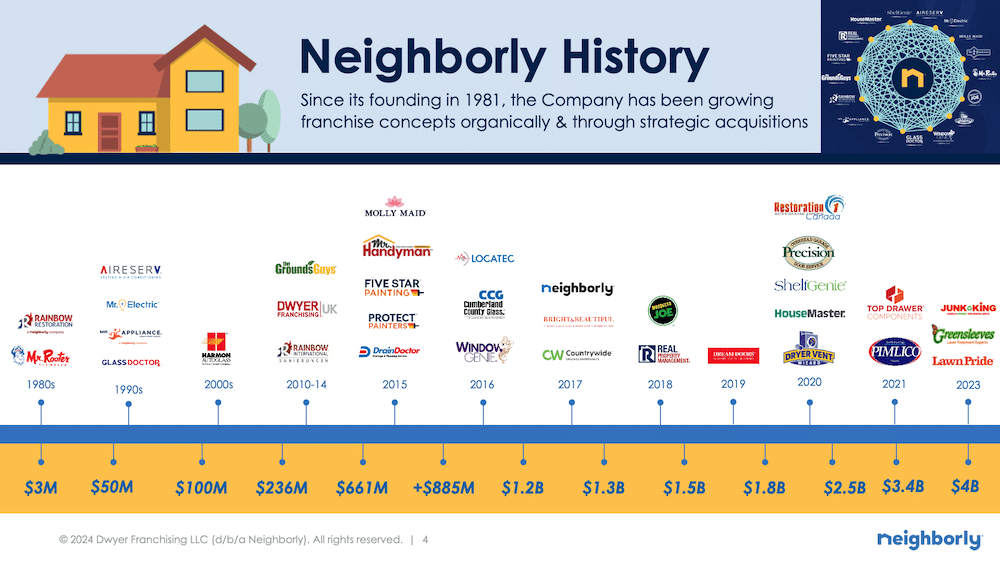

All the above didn’t happen overnight. Beyond operational scale, we were surprised to learn Neighborly’s tenure. It’s been in operation since the 1980s, starting with Rainbow Restoration and Mr Rooter. From there it grew over four decades, while assembling several more brands and ratcheting up its revenue.

That brings us to the present, where Stevenson paints a favorable picture of the macro-environment where it operates. For example, the average U.S. house is now 43 years old as newer construction has decelerated. This creates an environment that favors fixing and renovating over buying.

Amplifying that last part is the macroeconomic environment. With relatively high interest rates – even with the recent 50 basis-point Federal Reserve cut – homeowners are compelled to renovate versus move. This has been quite favorable to the home services industry, as we recently discussed with Yelp.

Going forward, Stevens sees even more growth, with demand for home services expected to grow by 49.4 percent between 2021 and 2028 according to Research and Markets. Altogether, Neighborly got our attention, and we’ll keep watching closely to see what growth avenues it pursues next.