Thryv held its investor day this week. And during a roughly two-hour session, it laid down some pretty aggressive markers for growing the company’s SaaS business over the next decade. Specifically, Thryv’s leaders said its SaaS business will reach $1 billion by 2027, and $4 billion by 2032.

By SaaS, we refer to subscription revenue from Thryv’s all-in-one business management software. This includes CRM, marketing automation, payments, document management, and a lot more.

To put this in perspective, Thryv closed out 2021 with $170.5 million in SaaS revenue. Its marketing services business, which is essentially the company’s print and online Yellow Pages business, pulled down $797.5 million. So in very rough terms, Thryv laid out a plan to flip its revenue mix in five years.

Thryv ended 2021 with 46,000 SaaS customers. By 2027, Thryv says that number will be 150,000, and by 2032, 500,000. This means customer growth will need to accelerate. And pretty dramatically for Thryv to reach these milestones.

Multi-pronged Approach

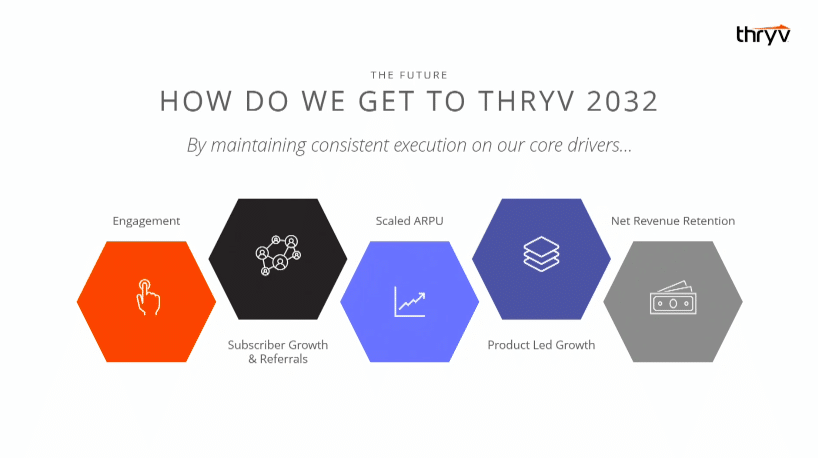

Thryv sees this happening through a combination of factors. One is accelerating penetration into what it calls “the zoo” or its existing marketing services customer base. And this is driven in large part by accelerating cloud adoption by existing customers. Thryv will also rely on more referrals from existing customers. And finally, it is rolling out new initiatives like product-led growth and a focus on franchise and multi-location businesses.

Speaking at the investor event, as well as in a phone call yesterday with Localogy Insider, Thryv CEO Joe Walsh made his case for why this level of SaaS growth is feasible. As Joe points out, this amount of growth is just barely enough for Thryv to maintain its current market share. That’s how big the opportunity is for Thryv, he says.

Thryv went public via direct listing last April. And its shares have been trading in a fairly consistent range. It debuted last April at 24.13 and peaked at 42.99 in January. It closed at 27.89 on Thursday.

Crossing the Chasm to the Cloud

Accelerating cloud adoption sits at the core of Joe’s case. He describes the small-business shift to the cloud as the “megatrend of all megatrends.”

He said Thryv was a bit early to the party with cloud adoption. And for the past several years, many of the company’s most loyal marketing services customers gave SaaS a hard pass.

He contends that now the long-anticipated, widespread small business shift to the cloud is finally happening. The pandemic was definitely an accelerant, but whatever the cause, “there is a change in the air,” Joe said. “Many customers that said no [to SaaS] for years, this year they are signing up.”

Localogy has measured small business SaaS adoption for years. We have generally found that older businesses with older owners are less willing to give up pen and paper in favor of cloud-based solutions. And Thryv’s customer base is long on established service businesses, many with older owners.

Joe says for whatever reason, those older owners have either come around to the need to modernize their businesses. Or they’ve decided to exit the business or bring in a younger decision-maker.

The net result is that many former repeated “No’s” are now becoming yesses, Joe said.

Tightening Up the TAM

A key to Thryv’s SaaS growth prospects is narrowing its focus on its best prospects. This means dramatically reducing its total addressable market. While this may seem counterintuitive at first glance it makes perfect sense. To grow, Thryv needs to retain and grow its customers. This is a lot harder to do if you sell to what Joe described in our call as “churn bombs.” These are companies that are relatively easy sales but very difficult renewals because they are highly unlikely to use the product.

Thryv used to see its U.S. TAM as roughly 8 to 10 million SMBs. Now it has reduced its TAM to about 4 million. This is out of roughly 30 million total U.S. small businesses. The insight that led Thryv to this conclusion is that engagement is its “North Star”. And to get the level of engagement that leads to higher retention and ARPU, Thryv can’t just sell to every “Chuck in a truck.”

“The business needs to be large enough to be a durable user of our product,” Joe said in his Investor Day presentation.

Thryv needs to increase its average revenue per customer significantly to hit its targets. Today it’s roughly $4,000. It needs to be roughly $5,000 to $6,000 in order to reach its targets.

Thryv CEO Joe Walsh ringing the NASDAQ bell earlier this week.

Going Global

Thryv plans to bulk its TAM back up by going global. Thryv already operates in the U.S., Canada, and Australia. The company estimates that there is another 8 million in TAM in the global markets it has its sights on. That is twice its revised U.S. TAM estimate.

Last year, Thryv acquired the Australian directories and local search company Sensis. It has since rebranded the company as Thryv Australia. And it has backed the rebranded up with a sizable ad campaign.

Thryv now plans to follow up on its Sensis acquisition with further international market entries. Joe was deliberately unspecific about where or how these market entries would take place. But we came away with the impression that things would happen fairly soon on this front.

At the Investor Day, the only clue Walsh gave on where it would expand was when he said, “We will go to the easy places.”

To us, this suggests developed English-speaking markets like the U.K. and New Zealand. We also imagine Western Europe is within the consideration set. Our sense is Thryv is more likely to ride into new markets on the back of acquisitions. The main reason we think this is that there are acquisition targets out there similar to Sensis at attractive prices. And acquisition is just an easier path to global expansion.

In our call, Joe did acknowledge there are clear advantages to entering international markets via acquisition. He said it allows a company to “scale and gain leadership quickly.” Sensis is a clear example of this.

‘I Love My Sales Force’

There was an extensive discussion of customer acquisition, both at the Investor Day and in our call.

As a local search business, Thryv has a sales-driven heritage. And it has historically seen its sales force as its greatest asset. And Joe says this belief has not fundamentally changed.

“I love our sales force,” Joe said in our call. “It is our not-so-secret weapon. And it is why we have such deep relationships with our customers. And such low churn.”

However, to grow its SaaS business, Thryv is expanding how it acquires customers, including the addition of a product-led-growth initiative.

Joe said this doesn’t mean Thryv will shift away from using a human sales force, both on-premise and telephone (now Zoom). He said PLG is about “finding hand-raisers and bringing them into our orbit.”

While he said the sales force will not get small, he does expect it to become more efficient, so Thryv won’t need to scale up the sales force as fast as it might need to without adopting methods like PLG.