We knew it would come this. With a gallon of regular gas costing $4.50 on average in my home state, Illinois, this was only a matter of time. You can now use the buy now, pay later model to fill up your tank.

Two leading BNPL platforms, Klarna and Zip, have announced partnerships with Texaco and Chevron to allow consumers to purchase gas and snacks via BNPL. They must repay in four installments within six weeks.

Klarna will require users to create a digital in-store card in the Klarna app. This is how Klarna is extending BNPL, originally a purely online payments model, into physical stores.

Sure we’ve seen the buy now, pay later model gradually adopt more and more use cases (B2B, travel, medical bills, etc.). But to us, gas now, pay later has a definite jump-the-shark vibe.

To validate our gut reaction, we turned to that font of collective wisdom, Twitter. Let’s just say the idea is getting a chilly reception in the Twitterverse. Here are a couple of typical reactions.

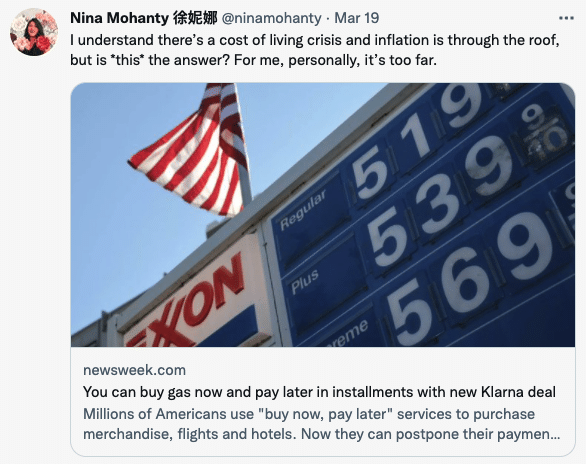

This user makes her point gently.

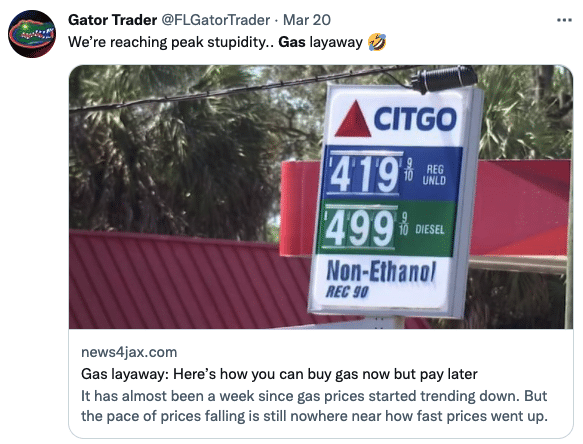

And this one, not so much.

So just in case it isn’t obvious, here is why this is such a sketchy idea. Gas is a frequent purchase item. Of course, people routinely use revolving credit cards to pay for gas. But the idea of creating a mountain of repayment obligation for such routine purchases is like building a house of cards in a wind tunnel. You just know it’s not going to end well.

If this catches on and cash-strapped consumers start using BNPL to fill up their tanks just to get to work, don’t be surprised if the “buy now, pay never” joke about BNPL starts to ring even more true than it does today.

Granted, regulators and legislators are pretty distracted these days. But we imagine someone from Congress or a regulatory agency will shine a light on this before long.