A new online banking startup called Hatch just announced it has raised $20 million from Kleiner Perkins, Foundation Capital, and others. What’s Hatch’s angle? The startup provides affordable banking services for cash-strapped solopreneurs, micro and small businesses. Its premise is that these businesses can’t stomach the roughly $450 they pay on average in annual overdraft charges.

Hatch’s founder and CEO Thomson Nguyen left Square in 2018 two years after selling the company his startup Framed Data. He then joined Kleiner Perkins as an entrepreneur in residence. That’s where he (pun intended) hatched the idea for his new company.

“More than 3.5 million small businesses have started in the US in the last year, with no signs of slowing down as we come into life post-COVID. These new small business owners take the risk to strike out on their own to build a better life for themselves, their families, and their communities,” Nguyen said in a company blog post announcing the fundraise and product launch.

“We sought out to build a business checking account with them in mind, with up to 5% debit cashback at gas stations, restaurants, and other businesses, no NSF fees, and up to $50 if your balance goes negative with Hatch Cover.”

What’s Hatch Cover? It’s a service that covers up to $50 on all eligible transactions if a customer goes negative on their account. And it does so without fees. More on Hatch’s products later.

Backed by Fintech Startpower

You learn a lot about a company by who puts money into it. And by these criteria, Hatch is worth watching. Nguyen launched (we won’t repeat the pun) the company in 2019, raising a $5 million seed round that year. in February 2020, right before the pandemic, Hatch raised a $14 million Series A round. According to TechCrunch, among those investing in the first two rounds were former Square executive Gokul Rajaram and Plaid founders William Hockey and Zack Perret.

Nguyen has also been able to build a leadership team with stints at some of the big names in fintech, including Stripe, Square, Bankrate, and others.

What’s a Neobank?

The neobank space is already pretty crowded. But most of the action has been focused on consumers. Companies like Chime, Dave, and a long list of others have popped up over the past few years to offer a new style of banking that appeals to younger and less-flush consumers. Hatch is bringing this vibe to the micro-business space.

Neobank is a term gaining some currency. It might help to offer a definition. We found this article that offers a helpful, though unofficial definition.

- A neobank has to be a pure startup. It cannot be a division of a major financial institution launched to target a new demo.

- A neobank must provide basic banking services, which it defines at minimum as an account with a routing number.

- It must operate 100% digitally. No physical branches.

By this definition, Hatch is certainly a neobank.

The main reason for neobanks’ appeal is not just that they offer banking in the cloud but also that they offer banking that doesn’t bleed the consumer or micro-business dry with fees. And they offer services that traditional banks have no interest in, like very small advances against future earnings. To give one example.

Again, Hatch is taking this movement to the micro-business, side-hustler space. Its sweet spot appears to be individuals who turned a pre-Covid side hustle into a main hustle once the Covid-related layoffs hit. A fair number of the 3.5 million small businesses launched last year likely fit that description.

In fact, as I was searching around to research this post, this appeared in my Facebook newsfeed.

Why Hatch?

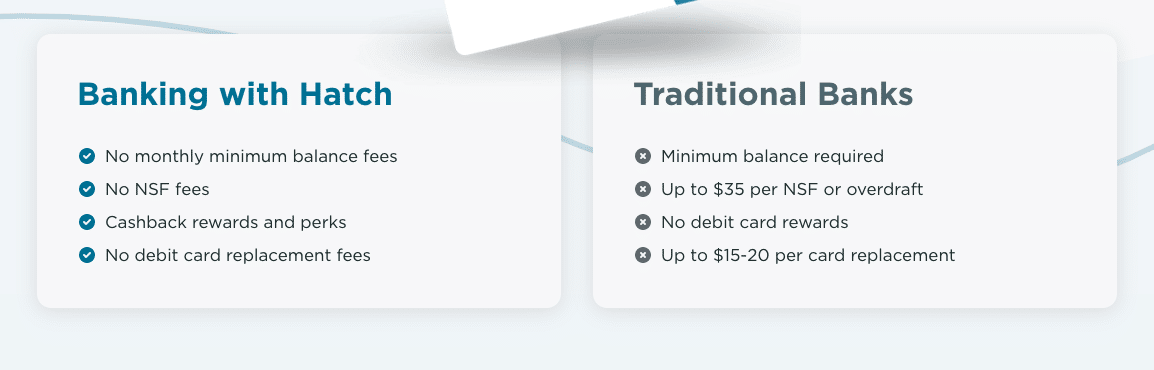

So what does Hatch offer, and why is it important to the small business space? For $10 a month a fledgling business can get a checking account that doesn’t nickel and dime with fees and offers cashback on purchases. Its new Cover feature, as noted, gives account holders some flexibility on overdrafts. The image below from Hatch’s website offers a comparison between Hatch and traditional banking.

Hatch also offers credit lines to eligible businesses. And the company is planning to launch something called Sprout, which will provide businesses with the basic elements of business formation — information, EIN numbers, and so on.

Hatch also offers credit lines to eligible businesses. And the company is planning to launch something called Sprout, which will provide businesses with the basic elements of business formation — information, EIN numbers, and so on.

Hatch seems like a product for the time. Covid appears to have accelerated another existing trend — the micro-business formed as much to make a living or to fit with a preferred lifestyle as to fulfill some entrepreneurial impulse.

Neobanks, whether aimed at consumers or side-hustlers (those lines are blurry to being with), are a real threat to traditional banks. Why pay all those fees when an online bank offers your the same for less? And with cooler branding. What began with young, tech-savvy consumers could become the norm among all demographics as well as small businesses sitting much higher on the ladder.

One thing saving traditional banks, in the near term at least, is that most neobanks lack an FDIC license and must partner with a traditional FDIC-insured bank to operate.